A minor pullback – is it already over?

Two weeks ago, we have raised the question “To correct or not to correct? After a minor pull-back in the broad market and sharp selloffs in highflyers like Tesla or GameStop broad market indices look from a technical standpoint ready for a next leg up. The RSI came down to a neutral territory and indices tested the 50-day average. This pullback happened without a significant rise in trading volume. By the contrary at lower market levels we have seen inflows into equity funds. Buy the dip is still the favorite strategy.

The pending US fiscal stimulus package which cloud be as high as 9% of US GDP, might push global GDP up by around 1-1.5%.

We had on top Fed Chair Powell testifying twice in front of US parliaments and twice during and after his speech US markets rallied. Lower for longer and the downplaying of inflation fears were enough to stabilize US equity markets.

Fig. 1: Nasdaq 100 trades after the pullback again above its 50-day average

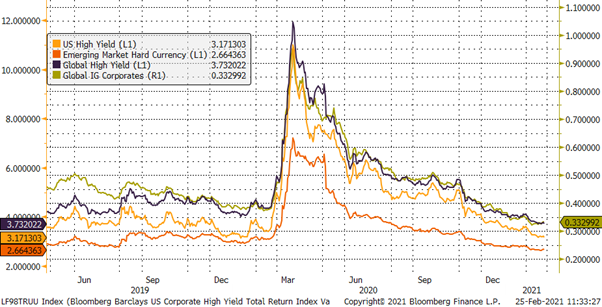

This minor pullback was accompanied by a massive rise in US 10-year treasury yields. Interesting is the decoupling of the US high yield and investment grade bond markets. Spreads so far have hardly moved and yields were range bound.

Fig. 2: Russel 2000 has consolidated without a significant pullback

Fig. 3: 10-year Treasury yields keep rising at a fast pace

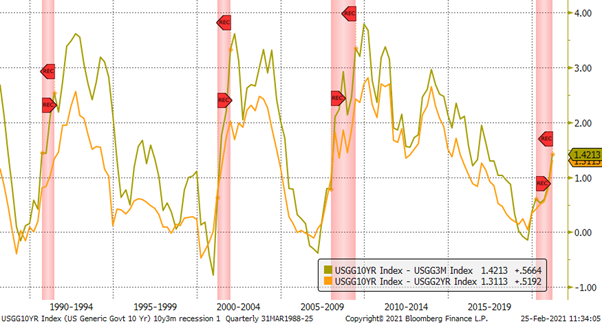

The US yield curve has steepened further as the yield levels from 1 month to around 7-year bucket have not moved much. We therefore get a clear signal from the US government bond market that the recession is behind us and that the growth outlook has significantly improved.

Fig. 4: Corporate bonds’ spreads did (so far) not react to rising treasury yields.

Fig. 5: The US yield curve has steepened and sends a clear signal that the US recession is behind us

Other macro indicators like the flash PMIs do confirm this view. The US data stayed in the acceleration area. Next week we get the next data set. It is expected that not only in the US but also in Europe we do see stronger PMI data, at least in the industrial area. The German ZEW or IFO indicators let us assume that the industrial sector has seen a strong increase of exports towards Asia. This picture is confirmed by a further rise of industrial metals.

Fig. 6: Copper continues to rise, indicating a strong increase of demand from industrials

The near future will depend on the impact of rising government bond yields on the corporate bond and equity markets. We expect that equity markets are resilient and will price in a stronger economy. The tech sector might continue to underperform cyclicals and small caps.

The bond markets must find a new balance between the yield level of corporates in relation to the relevant government bond markets. Therefore, the risk for rising yield spreads and a correction in corporate bond prices has risen.

Disclaimer: This Blackfort Insights (hereafter «BI») is provided for information purposes only. This document was produced by Blackfort Capital AG (hereafter «BF») with the greatest care and to the best of its knowledge and belief. Although information and data contained in this document originate from sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. Therefore, BF does not accept any liability for losses that might occur using this information. BI does not purport to contain all the information that may be required to evaluate all the factors that would be relevant for entering into any transaction and anyone hereof should conduct their own investigation and analysis. In addition, the BI includes certain projections and forward-looking statements. Such projections and forward-looking statements are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control. Accordingly, there can be no assurance that such projections and forward-looking statements will be actualized. The real results may vary from the anticipated results and such variations may be material. No representations or warranties are made as to the accuracy, or reasonableness of such assumptions, or the projections, or forward-looking statements based thereon. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted to access such information under local law. It may not be reproduced either in part or in full without the written permission of BF.

© Blackfort Capital AG. All Rights reserved.

Media about us:

-

-

Capital for The Energy-efficient Renovation of Swiss Homes

Uncorrelated earnings in Swiss Francs and more capital for the energetic refurbishment of Swiss houses – In the interview Wanja Eichl, Managing Partner, explains why Blackfort launches the new Swiss Real Estate Debt Fund. Please check it out via the following INTERVIEW Blackfort Swiss Real Estate Debt_e

-

More Capital for The Energetic Refurbishment of Swiss Real Estate

Contact us

Blackfort Capital AG Blackfort Schweiz AG

Talstrasse 61, 8001 Zurich Prime Tower, 8005 Zurich

Tel. +41 44 585 7878 Tel. +41 44 442 3202