Lockdown in Europe – but German IFO lead Indicators are on multiple years high

Lockdown in Europe – but German IFO lead Indicators are on multiple years high

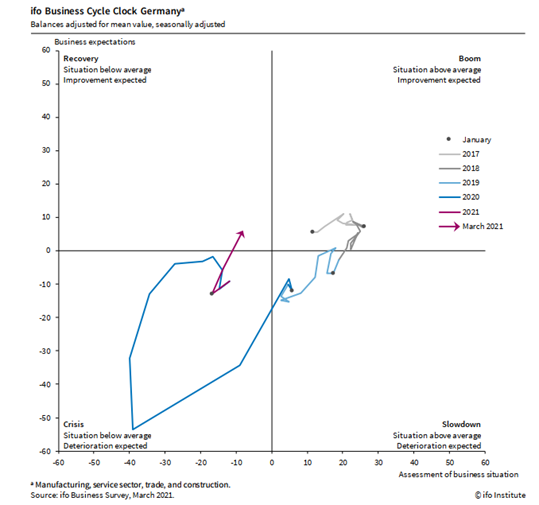

What a surprise: while Germany had its disastrous easter slow down announcement we had two press releases from the German IFO institute which stood in a stark contrast with the normal news flow. First, the business climate indicator rose to 22 months high bringing the IFO clock back to the recovery quadrant. But only to be followed by the release of the German export expectations which have reached a level last seen in January 2011.

These latest lead indicators not only confirm the recovery of the German export sector, but also confirm a pickup of growth in the Eurozone based on the latest strong flash PMI data. Market participants expect a strong global recovery later in 2021 once we will have vaccinated more than 50% of the population. At the beginning of April global PMI data will give us more insight regarding the future growth path.

Fig. 1: IFO Business clock back in recovery before re-entering the boom phase?

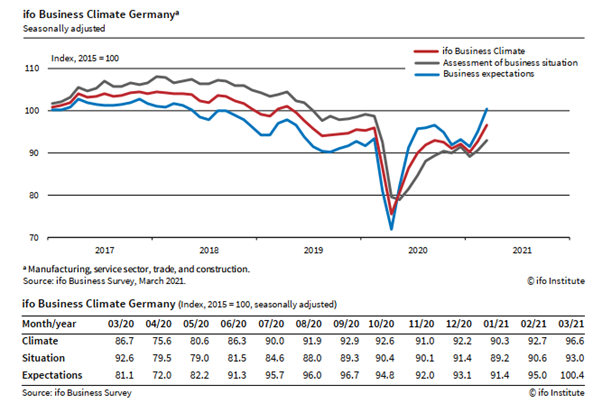

Fig. 2: IFO Survey: Strong business expectations, highest level in the last 22 months

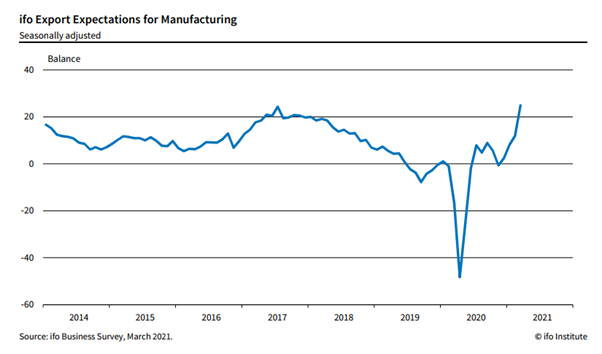

Fig. 3: IFO Export expectations on the highest level since January 2011

“A feeling of great optimism is emerging among German exporters. In March, the IFO Export Expectations in manufacturing rose from 11.9 points to 24.9 points – its highest level since January 2011. The export industry is benefiting from strong economic activity in Asia and the US. Momentum is slowly picking up again in the euro area, too.”

Source: IFO Institute

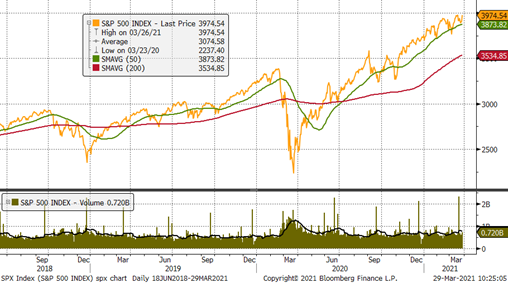

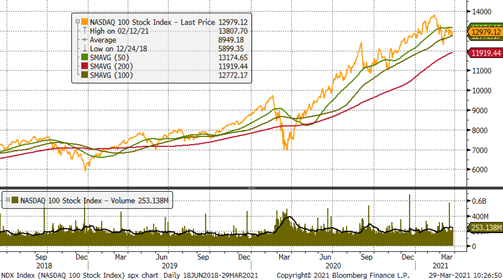

In the meantime, the market consolidation in both equities and bonds was ongoing. US tech have lost almost 10% during March while the broader market like S&P 500 lost less than 5%. Therefore, the S&P 500 trades above its 50-day average while the Nasdaq 100 is trading around its 100-day average.

Fig. 4: S&P 500 trades above its 50-day average

Fig. 5: Nasdaq 100 is testing its 100-day average

The question is – where are we going from here? We do expect a difficult US earnings season but would still expect that equities will perform better than bonds. Seasonality so far has worked out well during March with a strong start followed by a weaker 2nd half. If the script was to be continued, we should see a good April in equities.

We therefore stick to our equity allocation recommendation: to broadly invest in the US equity market as basis and to add small caps and tech stocks. We do as well overweight Asian equities where we have a bet on China A-shares and Vietnam.

Vietnam has just released its Q1 GDP estimation: Probably the country will grow 10% this year, which is one of the highest growth rate in our investment universe.

With such a strong global growth outlook we do expect that corporate bonds (mainly emerging market hard currency bonds and selectively US high yields) should deliver a positive return until the end of 2021.

Disclaimer: This Blackfort Insights (hereafter «BI») is provided for information purposes only. This document was produced by Blackfort Capital AG (hereafter «BF») with the greatest care and to the best of its knowledge and belief. Although information and data contained in this document originate from sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. Therefore, BF does not accept any liability for losses that might occur using this information. BI does not purport to contain all the information that may be required to evaluate all the factors that would be relevant for entering into any transaction and anyone hereof should conduct their own investigation and analysis. In addition, the BI includes certain projections and forward-looking statements. Such projections and forward-looking statements are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control. Accordingly, there can be no assurance that such projections and forward-looking statements will be actualized. The real results may vary from the anticipated results and such variations may be material. No representations or warranties are made as to the accuracy, or reasonableness of such assumptions, or the projections, or forward-looking statements based thereon. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted to access such information under local law. It may not be reproduced either in part or in full without the written permission of BF.

© Blackfort Capital AG. All Rights reserved.

Media about us:

-

-

Capital for The Energy-efficient Renovation of Swiss Homes

Uncorrelated earnings in Swiss Francs and more capital for the energetic refurbishment of Swiss houses – In the interview Wanja Eichl, Managing Partner, explains why Blackfort launches the new Swiss Real Estate Debt Fund. Please check it out via the following INTERVIEW Blackfort Swiss Real Estate Debt_e

-

More Capital for The Energetic Refurbishment of Swiss Real Estate

Contact us

Blackfort Capital AG Blackfort Schweiz AG

Talstrasse 61, 8001 Zurich Prime Tower, 8005 Zurich

Tel. +41 44 585 7878 Tel. +41 44 442 3202