Bi-Weekly. January 2021 I

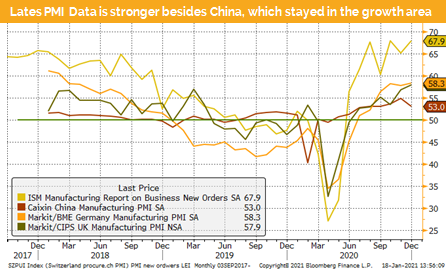

China’s latest data release conforms its strong economic recovery

Over the weekend China released a set of economic data. Unsurprisingly, based on leading indicators, its GDP grew in 2020 by 2.3%. Forth quarter GDP was stronger than consensus and the third quarter figure was revised up. This should come with little surprise, as the economy was growing in both quarters despite the COVID-19 measures.

China’s export statistics to Europe and within Asia have surged in Q4 2020. We won’t be surprised to see similar positive news from other Asian countries.

Meanwhile, president elect Joe Biden has announced a USD 1.9 trn rescue and recovery package. Amongst other things each citizen will get an unconditional USD 2’000 paycheck, or to be precise, an additional USD 1’400 to the recently distributed USD 600. This package is almost 10% of US GDP. Goldman Sachs has recently increased its US forecast to 6.2% from 5.8% only to be followed by another increase to 6.6% growth.

We stick to our assumption that the US and China will grow more than 6% in 2021, and we might get positive surprises across the globe.

From the vaccine front it looks like 3 new western vaccines in addition to the already 3 known ones will soon be available.

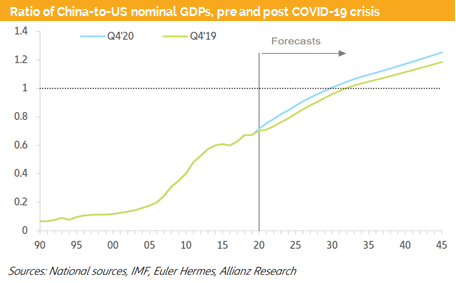

China and India together with Russia all have their own vaccine. The two Asian countries with the combined population of 2.5 bn, would probably recover from the pandemic sooner than expected. Asian economies will outpace the western world in 2021. It would mean that already in 3-5 years China’s economy will be bigger than the one of US.

This decade and may be even century will be led by Asian economies. We agree with it and expect that the US will do everything to catch up once they realize that they are losing their global economic leading position.

In Europe, the announced fiscal and monetary stimulus is still bigger than the US measures. However, we do not see the political will to reform the Eurozone. Also, large countries like Spain or Italy might just use the rescue money to finance their normal state, without implementing recovery measures. On top of that they have already announced that they are only interested in the unconditional part of the rescue package. This indicates that much needed reforms will be once again not implemented. Italy might even need a debt relief, as they are “too big to fail”.

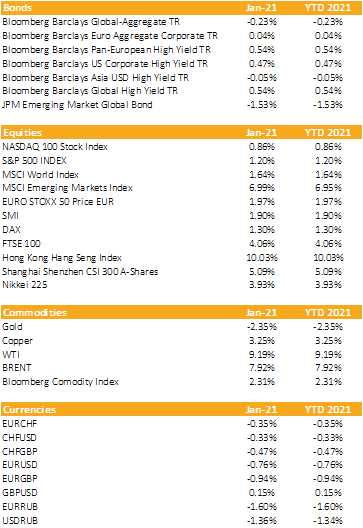

Currencies, Commodities, Equity & Bond Indices

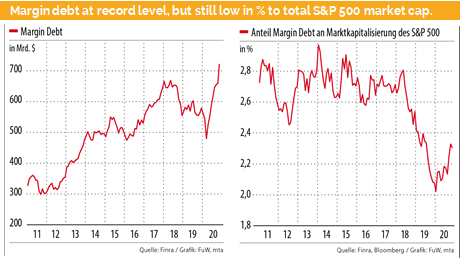

We do see more signs of euphoria in the US. Besides the already known robbinhood.com we see a new phenomenon – instead of the casino, retail investors bet now in stocks, for instance through wallstreetbets.

Another sign is the buying of stocks on margin has reached its highest level in history in absolute terms. Relative to the total market cap of the S&P 500 we are still below the 2014 peak. Nevertheless, the US stock market trades now at a higher PE than in 2014.

Another “betting place” is in cryptocurrencies with bitcoin leading the pack. In September 2020, the price was around USD 10’000, which followed by a surge straight up to USD 41’600 at the beginning of January. After we have seen a drop to around USD 36’000. Definitively these price moves have nothing to do with the fundamentals. We can however not rule out that this folly will last, and we could therefore see much higher prices during 2021.

Gold, on the other hand, is out of favor. Although we have more fear of inflation the gold price trades lower in a volatile environment.

Risk-on mode continues, but a pullback can occur any time

Liquidity

CHF: The Swiss franc trades in a narrow trading range sideways against USD and EUR. Recently the Euro is at the lower range and the SNB might intervene.

The EUR has weakened against the USD but still trades around 1.21.

The USD has strengthened since the beginning of the 2nd trading week. We expect that Mrs. Yellen, the new treasury secretary, will announce additional fiscal measures, and the dollar should therefore weaken further.

Equities

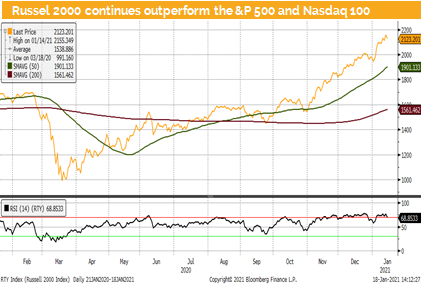

Most global equity markets are overbought. So far since November 2020 the equity market followed a typical seasonal path, with rising prices. The next chapter in the script would be a pullback followed by another leg up into spring.

As we do see a lot of complacency among professional investors and euphoria among retail investors, we cannot rule out that this folly continues without a pullback. Nevertheless, in the past exaggerations were always corrected.

The market got however more fuel due to the recent recovery and rescue package in the US. Republicans have already pushed back, and we might only see it to be implemented partially. It seems that both parties agree on a higher unconditioned paycheck for all citizen, which would give retail investors more cash to bet on wall street.

Fixed Income

US treasury yields surged in 2021. The 10-year yield went up from 0.9% to 1.15% and is now consolidation around the 1.1% level. Meanwhile US corporate bonds traded slightly higher. This is remarkable as on one hand in 10-year treasury the loss since the binging of the year is around 1.5% while during the same period US high yield bonds gained around 0.5%.

The elephant in the room is the expected rise in inflation and its impact on yields. We still expect that the Fed will not only hold its policy rate steady but also keep the yield of longer treasuries at artificial low levels through its bond purchasing program (aka financial repression).

Market participants expect that the 10-year yield will stay below 1.5% during the coming months and therefore should not hurt the economic recovery.

Alternative Investments

Gold: After the recent sell-off gold trades for the 2nd time during this consolidation at its 200-day average. We continue to believe that Gold will deliver protection against expected market turbulences.

REITS: Both commercial and residential real estates were rising together with equity markets. We still see more downside protection in residential REITS.

Oil: WTI oil futures have risen around 8% in 2021. The main reasons are the agreement among the OPEC+ countries to cut production and the expected global economic recovery

Investments covered:

Credito Real

Marfrig Global Foods

Gaungxi Investment Group

Elektra Group

Murphy Oil USA

Samsung Electronics

Disclaimer:

This Market Watch (hereafter «MW») is provided for information purposes only. This document was produced by Blackfort Capital AG (hereafter «BF») with the greatest care and to the best of its knowledge and belief. Although information and data contained in this document originate from sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. Therefore, BF does not accept any liability for losses that might occur using this information. MW does not purport to contain all the information that may be required to evaluate all the factors that would be relevant for entering into any transaction and anyone hereof should conduct their own investigation and analysis. In addition, the MW includes certain projections and forward-looking statements. Such projections and forward-looking statements are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control. Accordingly, there can be no assurance that such projections and forward-looking statements will be actualized. The real results may vary from the anticipated results and such variations may be material. No representations or warranties are made as to the accuracy, or reasonableness of such assumptions, or the projections, or forward-looking statements based thereon. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted to access such information under local law. It may not be reproduced either in part or in full without the written permission of BF.

© Blackfort Capital AG. All Rights reserved.

Media about us:

-

-

Capital for The Energy-efficient Renovation of Swiss Homes

Uncorrelated earnings in Swiss Francs and more capital for the energetic refurbishment of Swiss houses – In the interview Wanja Eichl, Managing Partner, explains why Blackfort launches the new Swiss Real Estate Debt Fund. Please check it out via the following INTERVIEW Blackfort Swiss Real Estate Debt_e

-

More Capital for The Energetic Refurbishment of Swiss Real Estate

Contact us

Blackfort Capital AG Blackfort Schweiz AG

Talstrasse 61, 8001 Zurich Prime Tower, 8005 Zurich

Tel. +41 44 585 7878 Tel. +41 44 442 3202